After two years of venue fights, narrowing motions and document skirmishes, the bank’s formal response to Palomino, Azteca and Appaloosa reads less like a counter-story than a litigation strategy

Credit Suisse’s formal answer in New York denies allegations that its final liquidity assurances misled AT1 investors

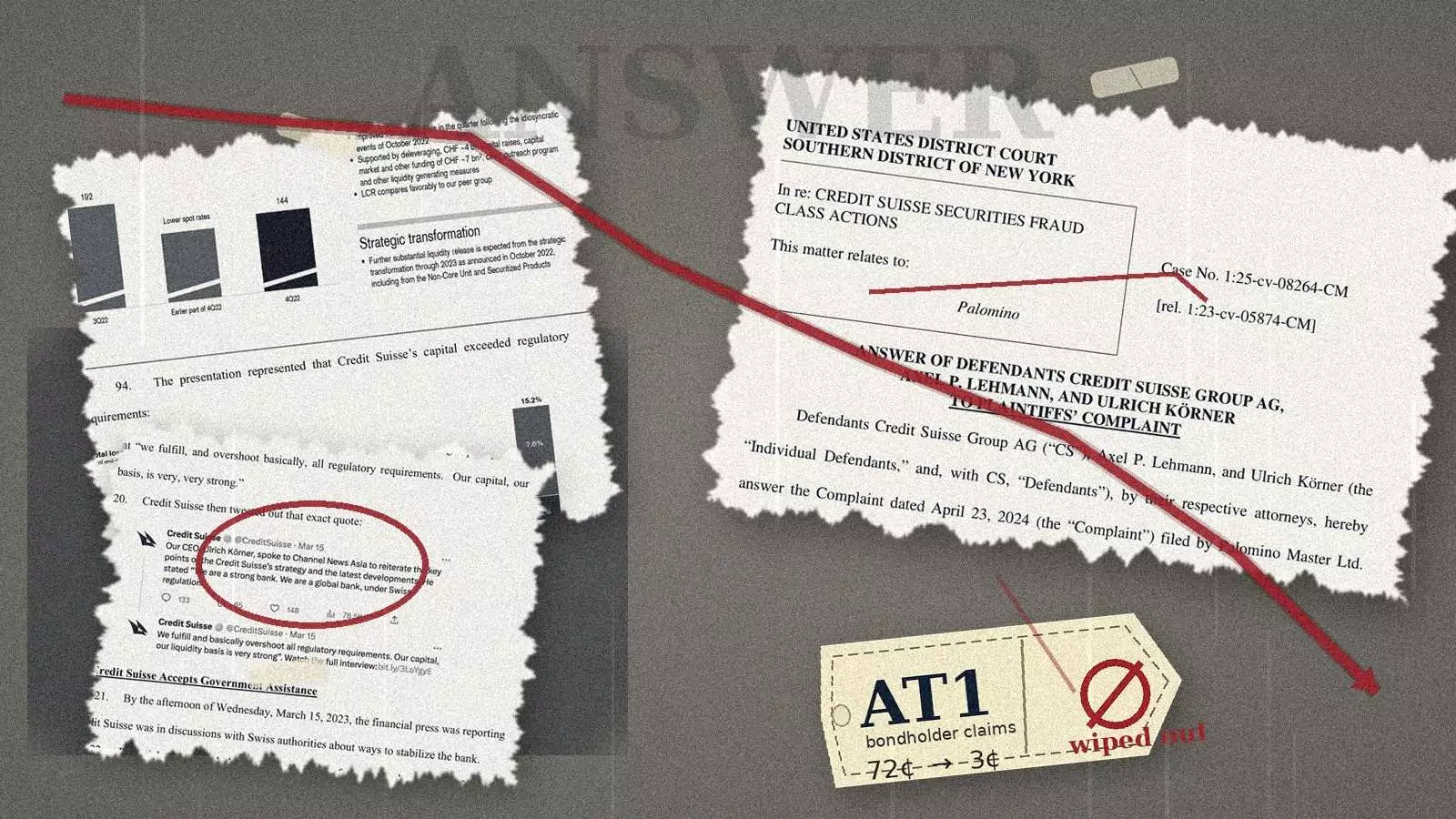

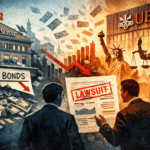

Credit Suisse’s formal response has now landed — and it is a revealing document. In an answer filed in Manhattan on April 9, Credit Suisse Group, former chair Axel Lehmann and former chief executive Ulrich Körner responded to the complaint filed on April 23, 2024 by Palomino Master Ltd., Azteca Partners LLC and Appaloosa LP over the wipeout of Credit Suisse’s AT1 bonds. The suit first surfaced in Reuters and Bloomberg, while the broader legal aftershocks of the rescue were later traced by the Financial Times. Strictly speaking, the new filing also shows how much the case has already been cut back: Appaloosa is no longer a plaintiff on the surviving claims because the New Jersey RICO theories to which it was tied have already fallen away.

What the defendants have filed, however, is not a full-bodied competing narrative of those days in March 2023. It is a wall of denials. Again and again, the answer says that the Bloomberg interviews, the Riyadh remarks, the fixed-income investor presentation, the FINMA materials and the executives’ later public comments “speak for themselves”; just as often, it says the plaintiffs’ “characterizations” are denied. For a filing that runs 53 pages, it offers remarkably little by way of a clean factual answer to the plaintiffs’ central charge: that Lehmann and Körner sold reassurance to the market when Credit Suisse’s liquidity position was already breaking down.

The road to this answer has already been long and, from the plaintiffs’ perspective, distinctly favourable to the defence. The complaint was filed in New Jersey in April 2024. Defendants then secured a stipulation under which they would not have to answer or otherwise respond until after their transfer motion was decided, and in June 2024 they formally moved to send the case to the Southern District of New York. That transfer was granted in January 2025 and affirmed on appeal in September 2025. Only after the case reached Manhattan did the defendants move to dismiss, winning the removal of the New Jersey RICO counts in March this year while leaving the federal securities claims alive. Crucially, Judge Colleen McMahon said those securities claims survived because the defendants had not challenged falsity, scienter or materiality at that stage. As reported after the March 26 ruling, the court kept the core fraud theory standing. None of this is improper. But it is hard to miss the practical effect: time was bought, forum was changed, and the complaint was narrowed before any merits answer arrived.

The same pattern is visible on disclosure. In the related AT1 bondholder litigation, the court allowed the case to move into discovery in July 2025. But when plaintiffs later sought certain Credit Suisse communications with FINMA, the route to production ran through further consultation with the Swiss regulator. A December 9 order recorded that a list of communications would be presented to FINMA so it could say whether each could be produced. A second order on December 18 said FINMA had consented, with restrictions, to the production of seven communications, after which the motion to compel was administratively closed. That record stops short of proving bad faith. It does, however, reveal a defence instinct for sequencing, narrowing and controlling access to the paper trail — an instinct we already criticised and which echoed earlier disputes over Swiss file access, including FINMA’s effort to keep records from bondholders and Credit Suisse’s opposition to document disclosure in Switzerland.

The plaintiffs’ case, by contrast, still draws its force from the compression of time. On March 14, 2023, Körner told Bloomberg that Credit Suisse had seen “material inflows” the previous day and described the bank’s liquidity coverage ratio as “strong, very strong” and “getting stronger”. The same day, a fixed-income presentation pointed investors to a 144 per cent LCR at year-end, capital above regulatory minimums, a loss waterfall in which AT1 capital sat above common equity, and a Swiss resolution regime said to enforce a “strict and complete hierarchy of losses”. On March 15, Lehmann said Credit Suisse had already “taken its medicine” and that government support was “not a topic whatsoever”. That evening, after Saudi National Bank chair Ammar Al Khudairy publicly ruled out further help, Körner again said the bank’s capital and liquidity were “very, very strong”. Hours later, Credit Suisse announced that it intended to borrow up to CHF50bn from the Swiss National Bank. Three days later came the state-backed sale to UBS and FINMA’s order to wipe the AT1 bonds to zero. FINMA’s March 15 statement with the SNB, Credit Suisse’s March 16 liquidity release, FINMA’s March 19 rescue release and its March 23 explanation of the AT1 write-down are the official bookends to that extraordinary week.

This is why the complaint remains, at least on first reading, more persuasive than the answer. The plaintiffs are not asking the court to infer fraud from a slow deterioration stretched across quarters. They are asking it to look at a 48-hour gap between reassurance and collapse. FINMA’s own December 2023 report said there was an “imminent threat” of Credit Suisse becoming insolvent in mid-March and described deposit outflows accelerating from CHF1.6bn on March 13 and CHF2.7bn on March 14 to CHF13.2bn on March 15, then CHF17.1bn and CHF10.1bn on the following two days. The same report said Credit Suisse told the SNB on March 16 that it could not secure enough liquidity through markets or other means. The complaint then pairs those figures with the executives’ later remarks at the bank’s final annual meeting — Körner calling Credit Suisse “particularly vulnerable” and Lehmann saying he believed in a successful turnround only “until the beginning of the fateful week”. Read together, that sequence makes “material inflows” and “not a topic whatsoever” look less like ordinary corporate optimism than like statements a court may ultimately find very difficult to square with the contemporaneous record.

There is another allegation in the complaint that is especially suggestive because it is so visual. The March 14 creditor deck did not simply present capital ratios. It also reminded investors that AT1 capital was “senior” to CET1 capital and invoked the “no creditor worse off than in liquidation” principle. Five days later AT1 holders were wiped out while shareholders still received UBS stock. FINMA has consistently defended the write-down, saying the contractual viability trigger was met and the Federal Council’s emergency ordinance gave it the authority to act. But in October 2025 Switzerland’s Federal Administrative Court said the write-off lacked legal basis and revoked FINMA’s decree in a partial decision; FINMA has appealed. That Swiss ruling does not decide the New York fraud case. It does, however, make the plaintiffs’ scepticism about what investors were told in the final days look less theatrical and more grounded. UBS’s own March 19 merger release and the later Swiss court rulings now sit awkwardly beside the language investors were shown on March 14.

The defendants’ answer meets all this with a familiar litigation toolkit. It admits the hard facts that cannot sensibly be denied: Credit Suisse suffered heavy withdrawals in October 2022; UBS agreed on March 19, 2023 to acquire the bank in an all-share transaction accompanied by a CHF9bn federal loss-protection package; and FINMA instructed Credit Suisse to write the AT1 bonds down to zero. But on the central issues the response retreats into affirmative defences: lack of standing, no material misstatement, no scienter, no reliance, no loss causation, truth supposedly already in the public domain, losses allegedly caused by third parties or market forces, non-actionable opinion or puffery, no control-person liability for Lehmann and Körner, and even a Morrison argument that the transactions fall outside the territorial reach of US securities law. This is classic defence pleading. It is also telling. The filing is strongest where it moves the fight away from what Lehmann and Körner actually said in those hours and towards standing, reliance, causation and forum.

It is weakest where investors will want the simplest answer. If March 13 brought “material inflows”, why did FINMA later describe CHF1.6bn of outflows? If government help was “not a topic whatsoever”, why did the official FINMA-SNB statement leave the door open to emergency liquidity the same day, and why did the bank itself announce up to CHF50bn of SNB borrowing before markets opened the next morning? The answer does not really confront those contradictions. It mostly refuses the plaintiffs’ framing and asks the court to read the underlying materials more sympathetically. That may yet prove enough as litigation tactics. As a factual rebuttal, it looks thin.

For now, then, the formal answer changes less than its filing date might suggest. After transfer skirmishes, a partially successful dismissal motion and disclosure fights, the essential question remains the same one that first animated the complaint in 2024: were Credit Suisse’s last public assurances an honest attempt to calm a panicked market, or a final act of misdirection before the trapdoor opened beneath AT1 investors? In Manhattan, that question has not been answered. It has only been preserved. And the defendants’ new filing, for all its length, reads more like an exercise in postponement than in explanation.

0 Comments